Featured

Table of Contents

Common approaches consist of: Personal loansBalance move credit cardsHome equity loans or lines of creditThe goal is to: Lower interest ratesSimplify regular monthly paymentsCreate a clear benefit timelineIf the new rate is meaningfully lower, you minimize total interest paid. Many credit cards provide:0% initial APR for 1221 monthsTransfer charges of 35%Example: You move $10,000 at 22% APR to a 0% card with a 4% transfer charge.

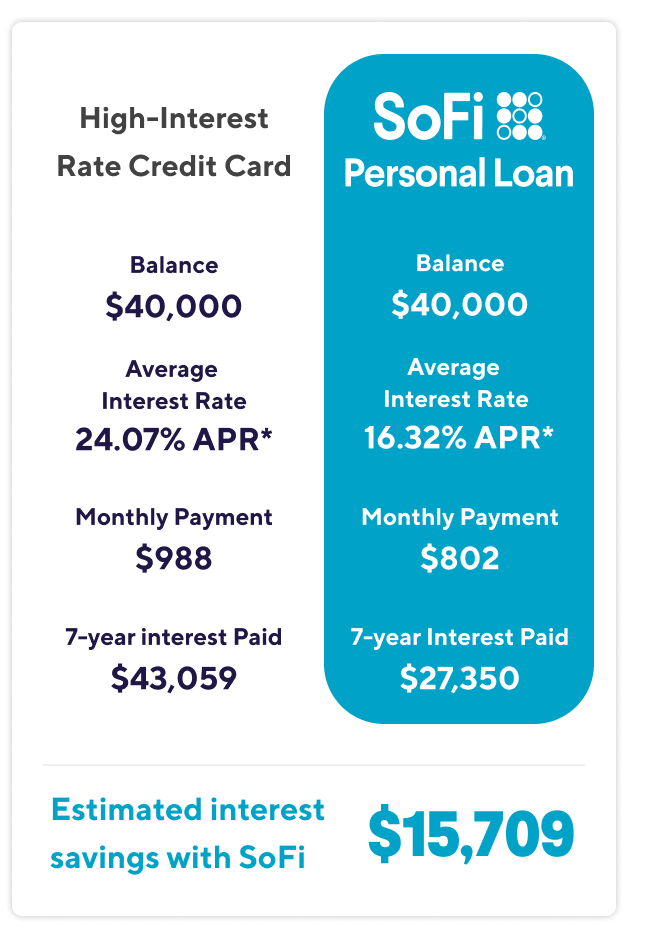

This works well if: You get approved for the credit limitYou stop including new chargesYou settle the balance before the advertising duration endsIf not settled in time, rates of interest can jump greatly. Balance transfers are effective but need discipline. A fixed-rate individual loan can change numerous card balances. Benefits: Lower rates of interest than credit cardsFixed monthly paymentClear payoff dateExample: Replacing 22% APR credit card financial obligation with a 912% individual loan significantly reduces interest expenses.

This shifts unsecured credit card financial obligation into protected debt tied to your home. Consolidation might be beneficial if: You certify for a considerably lower interest rateYou have steady incomeYou devote to not accumulating new balancesYou desire a structured repayment timelineLowering interest speeds up benefit but just if spending behavior modifications.

Before combining, determine: Current typical interest rateTotal staying interest if settled aggressivelyNew rate of interest and total cost under consolidationIf the mathematics plainly favors combination and habits is managed it can be tactical. Debt consolidation can briefly affect credit history due to: Tough inquiriesNew account openingsHowever, with time, lower credit utilization often improves ratings.

The Future of Debt Debt Consolidation in Your RegionGetting rid of high-interest financial obligation increases net worth straight. Moving balances however continuing spendingThis produces 2 layers of financial obligation. Picking long repayment termsLower payments feel easier but extend interest exposure.

How Professional Guidance Simplify Payments in 2026

Closing accounts can increase credit usage and affect score. Rates might not be significantly lower than existing credit cards. Credit card debt consolidation can speed up payoff but only with discipline.

Automate payments. Combination is a structural improvement, not a behavioral treatment.

It can be daunting when your charge card financial obligation starts to surpass what you can pay, particularly given that sometimes all it takes are one or 2 errors and quickly you're handling numerous balances from month to month while interest starts to accumulate. Credit card debt consolidation is one kind of relief offered to those having a hard time to settle balances.

2026 Reviews of Credit Counseling Plans

To get away the stress and get a manage on the financial obligations you owe, you require a debt repayment gameplan. In a nutshell, you're seeking to discover and collect all the financial obligations you owe, discover how debt consolidation works, and set out your choices based on a full assessment of your debt circumstance.

Balance transfer cards can be a great form of debt consolidation to think about if your debt is concerning however not frustrating. By making an application for and getting a new balance transfer charge card, you're essentially buying yourself additional time usually somewhere in between 12 and 21 months, depending upon the card to stop interest from accumulating on your balance.

Compared to other debt consolidation alternatives, this is a relatively simple method to comprehend and achieve. Many cards, even some rewards cards, use 0% APR marketing periods with zero interest, so you may be able to tackle your full debt balance without paying an additional cent in interest. Moving financial obligations onto one card can also make budgeting simpler, as you'll have less to keep an eye on each month.

The Future of Debt Debt Consolidation in Your RegionMany cards stipulate that in order to take benefit of the initial marketing duration, your debt needs to be moved onto the card in a certain timeframe, normally between 30 and 45 days of being authorized. Likewise, depending upon the card, you may need to pay a balance transfer cost when doing so.

How Nonprofit Guidance Manage Debt in 2026

Another word of care; if you're unable to repay the quantity you've transferred onto the card by the time to initial advertising duration is up, you'll likely undergo a much higher rate of interest than before. If you select to move on with this strategy, do everything in your power to guarantee your debt is paid off by the time the 0% APR duration is over.

This may be an excellent choice to think about if a balance transfer card appears best but you're unable to totally devote to having the financial obligation repaid before the rate of interest starts. There are several individual loan choices with a variety of repayment durations readily available. Depending on what you're eligible for, you might be able to establish a long-lasting strategy to settle your debt over the course of numerous years.

Comparable to stabilize transfer cards, individual loans might likewise have charges and high interest rates connected to them. Often, loans with the most affordable rate of interest are restricted to those with greater credit ratings a task that isn't simple when you're dealing with a lot of debt. Before signing on the dotted line, be sure to examine the small print for any charges or information you might have missed out on.

By borrowing versus your retirement accounts, generally a 401(k) or IRA, you can roll your debt into one payment backed by a retirement account utilized as security. Each retirement fund has particular rules on early withdrawals and limits that are vital to examine before deciding. What makes this choice possible for some people is the absence of a credit check.

Similar to a personal loan, you will have numerous years to pay off your 401k loan. 401(k) loans can be high-risk considering that failure to repay your debt and comply with the fund's rules might irreparably damage your retirement savings and put your accounts at threat. While a few of the rules and regulations have softened over the years, there's still a lot to think about and absorb before going this route.

Smart Strategies for Managing Card Debt in 2026

On the other hand, home and vehicle loans are classified as protected debt, because failure to pay it back might mean repossession of the asset. Now that that's cleaned up, it is possible to consolidate unsecured financial obligation (charge card debt) with a protected loan. An example would be rolling your charge card financial obligation into a mortgage, essentially gathering all of the balances you owe under one financial obligation umbrella.

Safe loans likewise tend to be more lax with credit requirements considering that the used asset offers more security to the lender, making it less dangerous for them to provide you money. Mortgage in particular tend to provide the largest amounts of cash; likely enough to be able to consolidate all of your credit card financial obligation.

{kind=link}

Latest Posts

Utilizing Online Loan Calculators to Plan Finances

Benefits of Certified Debt Counseling in 2026

2026 Analyses of Debt Management Plans